Tech giant Amazon (NASDAQ: AMZN) has been a sensational long-term investment, thanks to the company’s apparent disregard for staying in its lane. It went from being an online store for only books to an e-commerce platform for everything. And then it even went beyond e-commerce to develop business operations for shipping logistics, digital advertising, cloud computing, healthcare services, and more.

Another company with an ever-widening business vision is Singapore’s Sea Limited (NYSE: SE). The company has an e-commerce platform and a video game division, and offers financial technology (fintech) services. And it’s not content to sit in its core Asian markets. Rather, it aspires to have a growing global operation.

Even though Sea stock is down 85% from its all-time high, I think it’s surprisingly a better buy than Amazon stock today. Here’s why.

But first, Amazon is still a great company

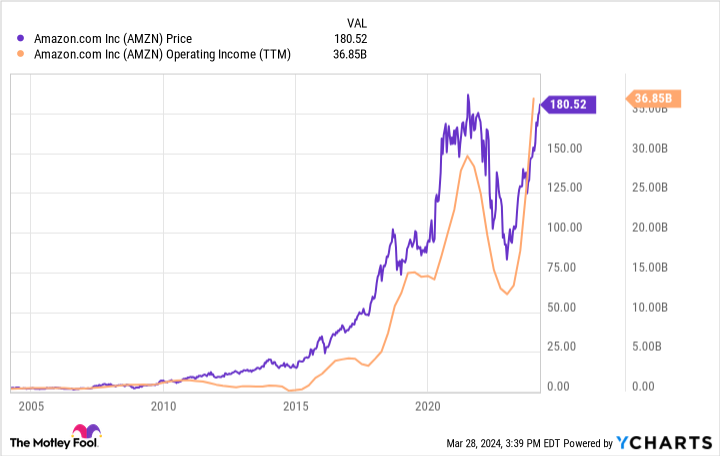

Don’t misunderstand: Amazon is still a great company. The stock is sitting near an all-time high thanks to its soaring operating profits. Indeed, the chart below shows a strong correlation between Amazon’s operating profits and its stock price over the last 20 years.

Over the last decade, Amazon’s operating profits have largely soared because of the success of its Amazon Web Services (AWS) cloud-computing services — AWS supplied 67% of the company’s operating income in 2023. But operating profits pulled back in recent years as it invested heavily in logistics to accommodate skyrocketing e-commerce demand.

Amazon’s operating profits are now normalizing as investments wind down. Management expects to earn $8 billion to $12 billion in the upcoming first quarter alone. Therefore, I wouldn’t be surprised if Amazon stock has more upside.

Compared to Sea stock, Amazon might be a safer bet for making money. That said, Sea stock could have more upside if things go right.

Why Sea stock is worth buying here

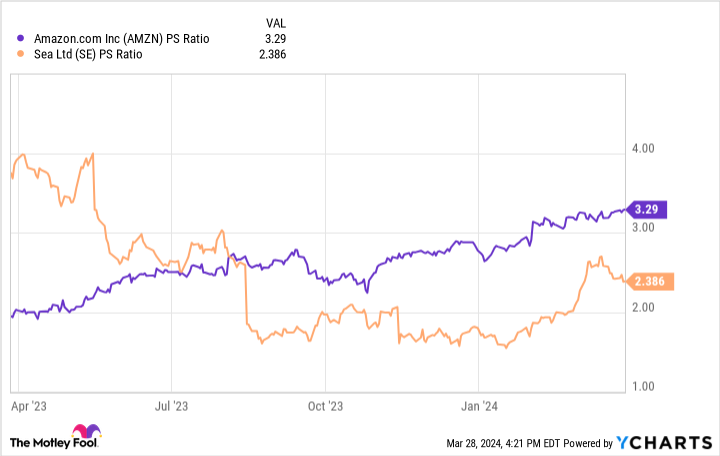

First, it’s important to note that Sea stock is cheaper than Amazon stock by the price-to-sales (P/S) metric.

To value a stock such as Sea at just 2 times sales suggests that investors don’t believe the company can grow — at least not profitably. But I think the company’s recent results disprove both opinions.

Consider the chart below that breaks down the financial results for all three of Sea’s business segments. Officially, the company calls these segments e-commerce, digital entertainment, and digital financial services. Note that the profit column refers to adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA).

|

Segment |

Revenue growth |

Profit |

|---|---|---|

|

E-commerce |

24% |

($214) million |

|

Digital entertainment |

(44)% |

$921 million |

|

Digital financial services |

44% |

$550 million |

Data source: Sea’s press release. Chart by author.

One of Sea’s segments has declining revenue, and another has an adjusted EBITDA loss. But as a whole, Sea’s revenue was up in 2023, and it was a profitable company. Therefore, the company can grow profitably because it’s doing it right now.

Therefore, the question isn’t whether this company can grow profitably; the real question is whether it can capture a large opportunity.

It’s hard to overstate the opportunities for Sea. The company does business in growing economies that are digitizing at a fast pace, such as Indonesia, Brazil, India, and more. And with these markets comes the potential for growth.

Take Sea’s focus on Brazilian e-commerce, for example. In 2020, the company entered the market. In February, just four short years later, it had already opened its 10th distribution center in the country.

These Brazilian distribution centers represent significant investment on Sea’s part. But as mentioned, it’s a big opportunity. Research group Mordor Intelligence estimates that Brazilian e-commerce is a $53 billion market today. But it predicts it will grow at an astonishing 19% compound annual growth rate through 2029. Other research groups similarly predict double-digit growth. And Sea is building the infrastructure to capitalize.

Sea is spending heavily on e-commerce. But it’s worth noting that its growth is becoming more sustainable. In 2023, the business segment did have an adjusted EBITDA loss of $214 million. But this was almost a $1.5 billion improvement, which shouldn’t be overlooked.

It’s not just e-commerce. Sea’s financial services division is obviously on fire. It expects a good year for its digital entertainment division as well in 2024, which is fueled by its hit game Free Fire. Management expects a return to double-digit growth this year and could soon relaunch in the massive market of India as it resolves regulatory issues.

With only $13 billion in trailing 12-month revenue, Sea has ample room for upside given the size of its markets, growth in those markets, and the strong demand for the products and services that it and its competitors offer.

With closer to $600 billion in trailing 12-month revenue, I’d say the upside potential for Amazon is much lower at this point, which is why Sea is a promising company for investors to consider buying today.

Should you invest $1,000 in Sea Limited right now?

Before you buy stock in Sea Limited, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Sea Limited wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of April 4, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Jon Quast has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Amazon and Sea Limited. The Motley Fool has a disclosure policy.

Love Amazon? This Alternative Stock Might Have Higher Upside. was originally published by The Motley Fool

")

{kind=link}