Micron Technology (NASDAQ: MU) wowed investors last week with an outstanding set of results for the second quarter of its fiscal 2024, reporting a massive jump in its revenue and a surprise profit, and this sent shares of the memory specialist soaring.

The chipmaker benefited from a jump in demand for memory chipsr. As a result, its revenue increased a massive 58% year over year to $5.8 billion. Micron is anticipating stronger year-over-year growth of 76% in its top line in the current quarter, driven by increased appetite for memory chips from artificial intelligence (AI) servers, smartphones, and personal computers (PCs).

The memory industry has witnessed a significant turnaround of late as demand for consumer electronics is back on track, while AI has created the need for advanced memory chips known as high-bandwidth memory (HBM). Micron management remarked on the latest earnings-conference call that its HBM capacity for 2024 is sold out, while the “overwhelming majority of our 2025 supply has already been allocated.”

This is good news for Lam Research (NASDAQ: LRCX), a semiconductor equipment manufacturer that gets a big chunk of its revenue from selling its goods to memory manufacturers such as Micron. Let’s look at the reasons why Micron’s latest results are an indication that investors would do well to buy Lam Research stock right now.

Lam Research is about to witness a solid turnaround

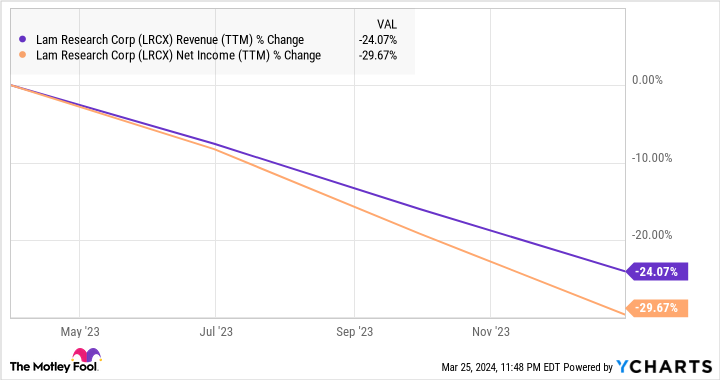

In the most recent quarter, Lam Research got 48% of its revenue from selling semiconductor manufacturing equipment to memory manufacturers. This explains why the company’s results in recent quarters have been poor. An oversupply in the memory market forced the likes of Micron and others to put a hold on capacity expansion, and so Lam’s top and bottom lines have been heading south.

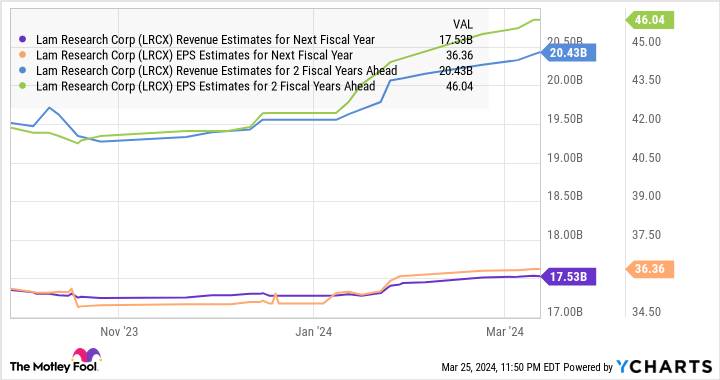

Analysts expect the company to finish the current fiscal year with a 22% decline in revenue to $13.6 billion. Additionally, earnings are expected to drop to $26.76 per share from $34.16. However, as the following chart shows, Lam Research’s revenue and earnings could jump sharply in the next fiscal year, which will begin at the end of June 2024.

Micron’s latest results and management commentary tell us just why Lam’s fortunes are set to turn around. Memory makers will need to increase their supply of HBM to cater to the growing demand from AI servers. The good part is that Lam is already witnessing solid orders for HBM equipment. CEO Tim Archer pointed out on the company’s January conference call with analysts: “In 2024, we expect our HBM-related DRAM and packaging shipments to more than triple year on year… “

It is also worth noting that the overall memory market is set to jump big time in 2024. According to Gartner, the memory industry’s revenue could jump 66% this year following a 39% drop in 2023. More importantly, the growing adoption of AI is set to drive robust long-term memory demand.

According to Micron, AI-enabled PCs are likely to carry 40% to 80% more DRAM (dynamic random access memory) content when compared to traditional PCs. On the other hand, the company expects AI-capable smartphones to “carry 50% to 100% greater DRAM content compared to non-AI flagship phones today.”

Meanwhile, the demand for HBM is forecast to more than double in 2024, generating $14 billion in revenue as compared to $5.5 billion last year. Even better, the HBM market could generate almost $20 billion in revenue next year. All this indicates that memory manufacturers will have to ramp up their production capacities, and a closer look at the industry indicates this is just what’s happening.

Samsung, for example, is expected to increase HBM production by 2.5 times in 2024, followed by a 2x increase next year. Similarly, SK Hynix expects to increase its capital expenditure this year to support increasing HBM demand. As such, the end-market conditions are set to turn favorable for Lam Research.

Buying the stock is a no-brainer right now

Lam Research is currently trading at 27 times forward earnings estimates. That’s a small discount to the Nasdaq-100‘s average multiple of 28 (using the index as a proxy for tech stocks). If Lam Research’s earnings hit the $46 estimate, and it were to trade at 28 times earnings, that would put its stock at $1,288, a 33% jump from its current price.

However, don’t be surprised to see the stock delivering stronger gains as the market may reward it with a higher earnings multiple thanks to its AI-fueled growth, which is why investors should consider buying this semiconductor stock before it jumps higher.

Should you invest $1,000 in Lam Research right now?

Before you buy stock in Lam Research, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Lam Research wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of March 25, 2024

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Lam Research. The Motley Fool recommends Gartner. The Motley Fool has a disclosure policy.

1 Semiconductor Stock to Buy Hand Over Fist After Micron Technology’s Stellar Report was originally published by The Motley Fool

")

{kind=link}