Happy talk from Washington, consistently low unemployment, and a slowing pace of inflation have combined to support a positive market sentiment – but can it last? ‘Shark Tank’ star Kevin O’Leary believes it won’t, and he does not hesitate to list the headwinds that could bring ‘real chaos’ by the year’s end.

The key factor is higher interest rates. The Federal Reserve has already pushed rates up to their highest level in over 20 years, and the repercussions are spreading. O’Leary takes special care to point out the effects on the commercial real estate market, where the increased rates imply that commercial mortgage loans – of which $1.5 trillion is due to turn over in the next few years – will refinance at nearly double their current interest rate.

With already more than $64 billion in troubled commercial real estate assets, O’Leary also notes that commercial mortgage delinquencies were up to 3% by the end of 1Q23. Additionally, small businesses, constituting around 60% of the US jobs market, are already strapped for cash and credit as banks and other financial institutions tighten lending conditions.

All of these factors add up to a situation that demands a defensive stance; investors will need to find protection for their portfolios. The logical move – and the classic defensive stock play – is a shift toward dividend stocks. These stocks, with their combination of passive income and lower average volatility, offer a shield against potential downturns.

Wall Street’s analysts have tagged two dividend-paying stocks as compelling ‘Strong Buy’ candidates with promising outlooks. Let’s take a closer look.

Brookfield Renewable Partners (BEP)

The first dividend stock we’ll look at is Brookfield Renewable Partners. Based in Bermuda, the company claims a global footprint of diverse energy assets. Its portfolio includes a wide range of distributed energy and sustainable operations. Additionally, it features more conventional green energy projects, such as wind, solar, and hydro-electric power generation systems.

The name ‘Brookfield’ should be familiar. It is one of the largest alternative investment firms in Canada, and Brookfield Asset Management owns a 60% interest in Brookfield Renewable Partners. This provides a solid financial underpinning for the energy company, allowing it to expand its power-generating facilities and operate at utility-grade scales.

Earlier this month, BEP released its financial results for the second quarter of 2023. Notably, the company experienced a 6.1% year-over-year growth in its funds from operations (FFO). Specifically, FFO surged from $294 million in the corresponding quarter of the prior year to an $312 million in 2Q23. Per share, the FFO amounted to 48 cents, which was 2 cents higher than in the prior-year quarter. The FFO supports the dividend here, which amounted to 33.75 cents per common share.

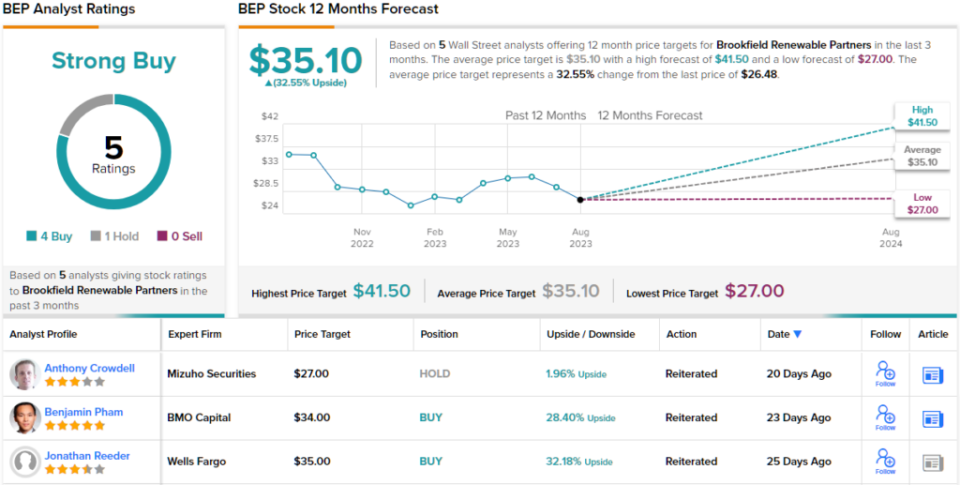

Turning to the dividend, we find BEP’s annualized rate of $1.35 per share and a yield of 5.1%. The dividend has been maintained without missing a quarter since 2018.

For Wells Fargo analyst Jonathan Reeder, the story on BEP is all about profiting from decarbonization. The analyst believes that BEP has positioned itself to survive a downturn.

“We continue to view BEP/BEPC as a compelling way for investors to play the global decarbonization movement. Brookfield has the ability to deploy capital—at scale—into traditional renewable assets as well as more strategic investments into businesses that are levered to the trends (i.e., Westinghouse and Origin). We believe BEP’s conservative strategy (IG balance sheet, highly contracted w/ inflation-linked revenues, etc.) is built to withstand macro challenges,” Reeder opined.

To this end, Reeder rates BEP shares an Overweight (i.e. Buy), while his $35 price target points toward a 32% upside heading out to the one-year horizon. (To watch Reeder’s track record, click here)

Most of the Wells Fargo analyst’s colleagues are on the same page. Based on 4 Buys and 1 Hold, BEP has a Strong Buy consensus rating. At $35.10, the average price target could provide investors with upside of ~23% in the coming months. (See BEP stock forecast)

Diamondback Energy (FANG)

Next up is Diamondback Energy, an independent oil and natural gas exploration and production firm based in Texas. Diamondback focuses on unconventional onshore plays in both oil and natural gas, engaging in activities such as acquisition, development, exploration, and exploitation of these energy sources, primarily in the Permian Basin of West Texas. Diamondback employs a strategy of horizontal exploitation to maximize the value extracted from each well.

The Permian Basin, where Diamondback concentrates its efforts, stands as the largest oil-producing sedimentary basin in the US. Over the past two decades, its high production has propelled Texas back onto the world map of petroleum producers. In the second quarter of this year, Diamondback achieved a daily average production of 449,912 barrels of oil equivalent, marking a 5.8% increase from the previous quarter and an 18% increase year-over-year.

Despite the growth in Diamondback’s gross production numbers, the company experienced declines in both revenues and earnings on a year-over-year basis. Total revenue amounted to $1.92 billion, representing a decrease of ~30% compared to the previous year. Similarly, the adjusted EPS figure of $3.68 per share was down from over $7 in the corresponding period of the previous year. However, both the 2Q23 revenue and EPS figures surpassed analyst forecasts, outperforming expectations by $26.19 million and 21 cents per share, respectively.

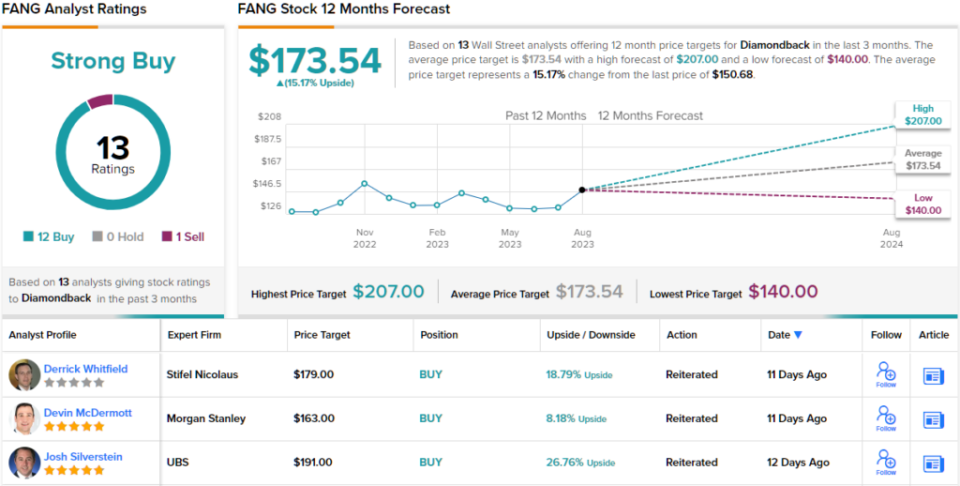

During Q2, Diamondback generated a free cash flow of $547 million. This figure should pique the interest of dividend investors as it directly supports the company’s capital return policy, which encompasses dividend payments and share repurchases. In Q2, Diamondback allocated $473 million for these purposes. The most recent dividend payment for Q2 was disbursed on August 17, amounting to 84 cents per share. Annually, this translates to $3.36 per share and yields a 2.2% return. The company has a history of adjusting dividend amounts to ensure coverage and has consistently distributed dividends since 2018 without missing a single quarter.

For RBC Capital’s 5-star analyst Scott Hanold, this company’s reliability is the point that investors should take note of. He writes of Diamondback, “Focus on stable operations is delivering consistent results that are slightly ahead of expectations. This underpins its strong FCF outlook that provided confidence to increase the fixed dividend. Incremental shareholder returns remain a decision based on the intrinsic FANG value that could move back to more variable dividends. We see good upside value in FANG shares in the current market, which generally warrants buybacks, but at mid-cycle oil prices, valuation is likely near the high end of the band.”

Hanold goes on to give FANG shares an Outperform (i.e. Buy) rating, while his price target of $170 implies a share appreciation of ~13% in the year ahead. (To watch Hanold’s track record, click here)

All in all, 11 other analysts join Hanold in the bull camp and the addition of one bear can’t detract from a Strong Buy consensus rating. The forecast calls for 12-month returns of 15%, considering the average target stands at $173.53. (See Diamondback stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

")

{kind=link}