Global tobacco giant Philip Morris International (NYSE: PM) has been stuck in the mud for five years. The stock has zigged-zagged up and down, but it currently sits roughly where it did in 2019.

But that could soon change. The company has been working hard to develop and acquire its next-generation products to drive the growth needed to take the stock to new heights.

Want to know more? Here’s why Philip Morris is a smoking-hot buy today.

Next-generation growth

Philip Morris cut its teeth selling Marlboro cigarettes in non-U.S. markets, but it has spent years developing new revenue streams that should eventually carry the business as people smoke fewer combustible products. Those are IQOS and Zyn. IQOS is a device that heats tobacco to produce a vapor but doesn’t burn the tobacco, decreasing the amount of toxins users inhale. Meanwhile, Zyn is an oral pouch that contains flavored nicotine powder.

The company launched IQOS in 2014 and has built the brand over the past decade. Today, 28.6 million users are on IQOS devices. It’s accumulated a 9.7% market share of all tobacco use in markets where IQOS is available, second only to Philip Morris’s Marlboro cigarette brand. IQOS will soon launch in the United States, a new market that Philip Morris previously didn’t have access to. There are an estimated 28 million smokers in the country, so it’s an excellent opportunity to compete with former sister company Altria, which owns the Marlboro name in the U.S.

Philip Morris bought Swedish Match in 2022 to acquire the Zyn brand. It’s the global leader in nicotine pouches, a rapidly growing product category. Trailing-12-month shipment volumes hit 385 million cans in Q4 2023, up 62% year over year. That volume growth is rare in the nicotine space, so it’s an exciting long-term development for investors.

The company hopes these next-generation products will contribute at least two-thirds of total revenue by 2030, up from 36.4% last year. There are over 1 billion smokers worldwide, and Philip Morris has a unique combination of leading brands and access to the global market.

A juicy dividend

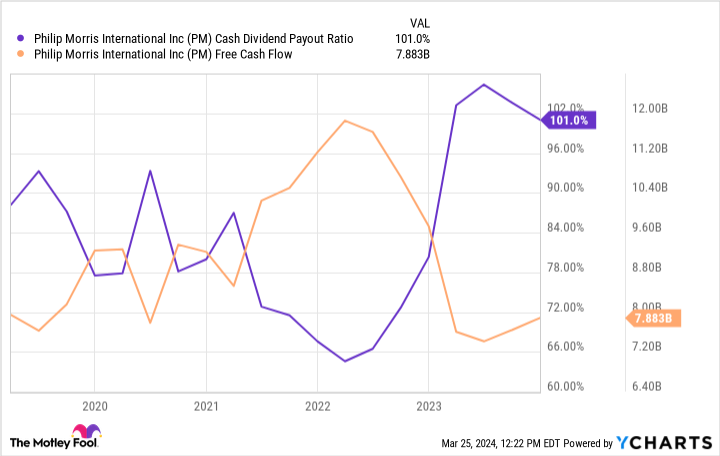

Tobacco stocks are famous for having big dividend yields, and Philip Morris fits the bill at 5.7%. Admittedly, the dividend payout ratio is tight at 101% of cash flow, but the company has invested heavily in growing Zyn’s capacity and sales since acquiring the brand in 2022.

As cash flow rebounds, that payout ratio should come down. Most importantly, investors are unlikely to see a dividend cut. Any dividend-paying company is reluctant to cut its payout, but tobacco management teams are especially reluctant to do so because they know dividends are the primary reason shareholders own the stock. If needed, management can tap the balance sheet to fill any gaps in the dividend payout. There was $3.1 billion in cash on the balance sheet at the end of 2023, and the company boasts an investment-grade credit rating.

Shares are priced for solid investment returns

The best way to profit from owning a stock like this is to buy, hold, and reinvest the dividends as they come. The dividends will compound over time, and investors can also enjoy some price appreciation.

Today, shares trade at a forward P/E ratio of 14, and analysts believe the company can grow earnings 7% annually over the next three to five years. Assuming the valuation remains the same, investors could see over 12% annual returns. The stock could be a little expensive; its PEG ratio is 2, and I like to buy stocks when the PEG is 1.5 or less. The PEG ratio tells investors how much they’re paying for that company’s earnings growth — lower is better.

However, long-term investors should see the company grow into its price tag. More importantly, looking five or more years out, Philip Morris could become a cash cow as Zyn investments fade and Philip Morris pays down some debt.

Eventual share repurchases could set the company up for prolonged earnings and dividend growth — just rinse and repeat.

Should you invest $1,000 in Philip Morris International right now?

Before you buy stock in Philip Morris International, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Philip Morris International wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of March 25, 2024

Justin Pope has no position in any of the stocks mentioned. The Motley Fool recommends Philip Morris International. The Motley Fool has a disclosure policy.

My Oh My, This 5.7% Yield Dividend Stock Is a Magnificent Buy was originally published by The Motley Fool

")

{kind=link}