-lose-their-trillion-dollar-market-caps-by-2026")

For the last 19 months, Wall Street has been a stomping ground for the bulls. All three major stock indexes have recently galloped to fresh record-closing highs, with opportunistic investors pouncing on any notable pullbacks.

While hot trends like artificial intelligence (AI) and stock splits have been widely credited with pushing the stock market to new heights, it’s the “Magnificent Seven” stocks that have done the majority of the heavy lifting.

The Magnificent Seven represent seven of the most influential and innovative businesses in the country and include:

-

Apple (NASDAQ: AAPL): $3.45 trillion market cap

-

Microsoft (NASDAQ: MSFT): $3.31 trillion

-

Nvidia (NASDAQ: NVDA): $3.02 trillion

-

Alphabet (NASDAQ: GOOGL)(NASDAQ: GOOG): $2.27 trillion

-

Amazon (NASDAQ: AMZN): $1.94 trillion

-

Meta Platforms (NASDAQ: META): $1.24 trillion

-

Tesla (NASDAQ: TSLA): $786 billion

Every Magnificent Seven component has handily outperformed the benchmark S&P 500 over the trailing decade. More importantly, these are business that possess well-defined competitive advantages, if not outright moats.

For example, Amazon, Microsoft, and Alphabet are the respective parent companies of Amazon Web Services, Azure, and Google Cloud, which collectively account for around two-thirds of global cloud infrastructure service spending. Meanwhile, Apple’s iPhone has earned a greater than 50% share of the domestic smartphone market, Tesla is North America’s undisputed leader in electric vehicle sales, and Nvidia shipped an estimated 98% of all graphics processing units (GPUs) used in high-compute data centers last year.

Long story short, there are tangible reasons why these are America’s leading businesses.

However, the outlooks for these seven companies differs quite a bit. If history tells us anything, it’s that Wall Street’s biggest companies by market cap are constantly being reshuffled over time. By 2026, it’s my prediction that two of the Magnificent Seven stocks, which currently possess trillion-dollar market caps, will fall below this psychological threshold.

Nvidia

The first Magnificent Seven stock that I foresee being knocked from its pedestal is the face of the artificial intelligence revolution, Nvidia. For Nvidia to lose its trillion-dollar market cap, shares would have to decline by about 67% over the next two years.

To put things into perspective, Nvidia was worth $360 billion when 2023 began. Shortly after the company completed its 10-for-1 stock split in June, it skyrocketed to a market cap of around $3.5 trillion. At its peak, Nvidia tacked on more than $3.1 trillion in value in under 18 months, solely because of its dominance in AI-accelerated data centers.

On one hand, there are viable reasons for investors to be excited about Nvidia’s role in the AI revolution. For instance, its H100 GPU has become the go-to chip for businesses wanting to train large language models and run generative AI solutions. When coupled with Nvidia’s CUDA platform, which is the toolkit developers use to build large language models, Wall Street’s AI darling has a distinct lure to keep clients within its ecosystem of products and services.

To add to the above, Nvidia has enjoyed nothing short of otherworldly pricing power for its AI-GPUs. With most top-tier tech companies aggressively investing in AI-driven data centers, Nvidia hasn’t been able to keep up with demand. This is typically good news for its pricing power and gross margin.

However, history has shown us time and again that the euphoria fades for hyped technologies that haven’t yet matured.

Since the advent of the internet roughly 30 years ago, there hasn’t been a game-changing innovation that’s avoided a bubble-bursting event. All technologies and trends need time to mature — and that includes artificial intelligence (AI). The simple fact that most businesses lack a clear-cut plan to generate a positive return on their AI investments suggests a bubble is brewing.

Additional confirmation that the AI bubble could burst sooner rather than later can be seen in Nvidia’s valuation. While it’s still reasonably priced relative to its forward-year earnings, Nvidia closed the July 23 trading session at 38 times trailing-12-month (TTM) sales. This is more or less on par with the TTM price-to-sales ratios seen from market leaders prior to the dot-com bubble bursting.

We’re also likely to see competitive pressures weighing on Nvidia’s adjusted gross margin in future quarters. The introduction of AI-GPUs from chief rivals Advanced Micro Devices and Intel, coupled with Nvidia’s top customers (Microsoft, Meta Platforms, Amazon, and Alphabet) all developing AI-GPUs for their respective data centers, will reduce the GPU scarcity that sent the company’s pricing power into the stratosphere.

Meta Platforms

The second Magnificent Seven stock that can, at least briefly, lose its trillion-dollar market cap is social media colossus Meta Platforms. Whereas Nvidia’s stock would need to plummet 67% to no longer be a trillion-dollar company, Meta’s stock would only have to decline by 19% to dip below this psychological level.

The biggest difference I see between Nvidia and Meta is that any significant pullback in Meta’s stock would represent an attractive buying opportunity. With AI still an immature technology, I can’t say the same about Nvidia given that the bulk of its valuation gain is tied to artificial intelligence.

Despite being incredibly bullish on Meta over the long run — it’s my third-largest stock holding — there are two reasons I believe we’ll see its stock briefly dip below $394, which would remove it from the trillion-dollar ranks.

First off, Meta generates close to 98% of its sales from advertising. Companies aren’t shy about paring back their advertising budgets at the first signs of economic turbulence. With U.S. M2 money supply notably declining for the first time since the Great Depression, there are signs that consumer spending isn’t as healthy as it seems. In other words, there’s a reasonable chance of a U.S. recession materializing by 2026. Even though recessions are short-lived, ad-driven businesses like Meta would probably take it on the chin if one occurs.

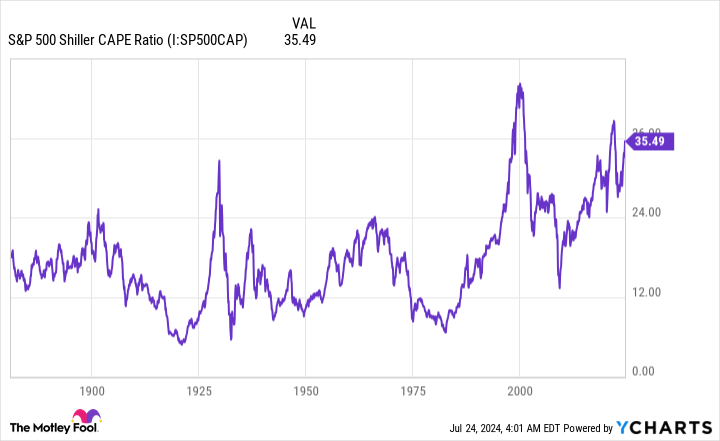

The other concern I have for Meta is the general priciness of the stock market. The S&P 500’s Shiller price-to-earnings (P/E) ratio, which is also known as the cyclically adjusted price-to-earnings ratio, or CAPE ratio, closed at nearly 36 on July 23. This is more than double its average, when back-tested to 1871.

More importantly, the previous five instances where the Shiller P/E surpassed 30 during a bull market over the last 153 years were eventually (key word) followed by a decline ranging from 20% to 89% for the S&P 500 and/or Dow Jones Industrial Average. Wall Street doesn’t tolerate extended valuations over the long run, which means the stocks that propped up the market at a premium (i.e., the Magnificent Seven) would likely be hit the hardest on the downdraft.

On the bright side, Meta is one of the cheapest Magnificent Seven components. It’s currently valued at 21 times forward-year earnings and is forecast to grow its earnings per share (EPS) by an annual average of 30% through 2028.

It’s also a company that’s swimming with cash. Meta closed out the first quarter with $58.1 billion in cash, cash equivalents, and marketable securities, and is on pace to generate over $76 billion in net cash from operations this year. This cash provides a healthy downside buffer for the company.

The cherry on the sundae for Meta is that no other social media platform comes close to attracting 3.24 billion daily active users across its family of apps. More often than not, this is going to provide Meta with exceptional ad-pricing power.

Even if Meta were to briefly lose its trillion-dollar market cap by or before 2026, it would mark a phenomenal buying opportunity.

Should you invest $1,000 in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $751,180!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of July 22, 2024

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Sean Williams has positions in Alphabet, Amazon, Intel, and Meta Platforms. The Motley Fool has positions in and recommends Advanced Micro Devices, Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla. The Motley Fool recommends Intel and recommends the following options: long January 2025 $45 calls on Intel, long January 2026 $395 calls on Microsoft, short August 2024 $35 calls on Intel, and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Prediction: These 2 “Magnificent Seven” Stocks Will (at Least Briefly) Lose Their Trillion-Dollar Market Caps by 2026 was originally published by The Motley Fool

")