A version of this post first appeared on TKer.co

Stocks closed higher last week with the S&P 500 climbing 0.4%. The index is now up 12% year to date, up 20.2% from its October 12 closing low of 3,577.03, and down 10.4% from its January 3, 2022 record closing high of 4,796.56.

On Thursday, we finally got confirmation that the bear market ended in October and that we’ve been in a new bull market ever since.

We’re also realizing this year’s market moves so far have been far outside consensus expectations in a bullish way.

Let’s turn back the clock.

An ‘overstated’ concern 🤏

In December, I published a roundup of Wall Street strategists’ 2023 outlook for stocks. The takeaway at the time: “Strategists expect a volatile first half to be followed by an easier second half, which could see stocks climb modestly higher.”

The big concern was that a brief earnings growth recession, which has sorta come to fruition, would come with renewed selling in stocks

But at the time, a handful of analysts, like Oppenheimer’s Ari Wald, ran the numbers and concluded “concerns are overstated.”

Not only is there a very weak linear relationship between one year’s earnings change and one year’s S&P 500 price change, but there’s actually some evidence that a trough in earnings is actually a lagging market indicator. Furthermore, history shows there are more instances when stocks didn’t fall but rose in years when earnings fell.

A ‘most popular’ concern 👯♀️

There was also the issue that many experts were openly calling for stock market weakness in the first half of the year. The prediction even made the cover of Barron’s!

At the time, two of the savviest Wall Street strategists I follow remarked on this. From the December 18, 2022 TKer:

“I do think that we are going to go down and then up… The problem is that is an increasingly consensus view. So I think the bigger risk heading into the first half is actually not being invested in equities.” – BofA’s Savita Subramanian, Dec. 7.

“Everybody and their mother, brother, sister, cousin, and uncle is negative on the first half of the year… So we’ll come out and be a little bit different. I think the weakness is probably not going to be as long as everybody thinks.” – BMO Capital Markets’ Brian Belski, Dec. 16

The thing about risks is that they become less of a problem for markets the more market participants talk about them because that means the risks are probably priced in.

Indeed, it’s mid-June and the stock market has spent the first five and a half months of the year mostly trending higher. The S&P 500 went modestly into the red on January 3 and 5; every other day it’s been in the green.

“The most popular prediction headed into 2023 was that markets would suffer through a rough first half but rally by year’s end,” Michael Arone, State Street Global Advisors, wrote on Tuesday. “However, stocks and bonds have refused to comply with the consensus forecast.”

In recent weeks, the consensus has shifted with strategists across Wall Street revising up their year-end price targets for the S&P 500, including Goldman Sachs’ David Kostin (to 4,500 from 4,000), BMO Capital Markets’ Brian Belski (to 4,550 from 4,300), BofA’s Savita Subramanian (to 4,300 from 4,000), and RBC Capital Markets’ Lori Calvasina (to 4,250 from 4,100).

The big picture 🤔

To be clear, this is not intended to be a celebration of bearish market-timers being wrong.

Rather, the point is that it is incredibly difficult to predict short-term moves with any accuracy, even when you know where the fundamentals are headed.

And it can be particularly dangerous to make bearish moves in a stock market that usually goes up. You risk missing out on significant short-term gains, doing irreversible damage to your potential long-term returns.

Reviewing the macro crosscurrents 🔀

There were a few notable data points and macroeconomic developments from last week to consider:

🛍️ Consumer spending is holding up. From Bank of America: “Bank of America internal data suggests consumer spending was broadly stable in May, with Bank of America total card spending per household up 0.1% month-over-month (MoM), seasonally adjusted. The year-over-year (YoY) growth rate remains negative at -0.2% YoY.”

From JPMorgan: “As of 04 Jun 2023, our Chase Consumer Card spending data (unadjusted) was 2.2% above the same day last year. Based on the Chase Consumer Card data through 04 Jun 2023, our estimate of the US Census May control measure of retail sales m/m is 0.46%.“

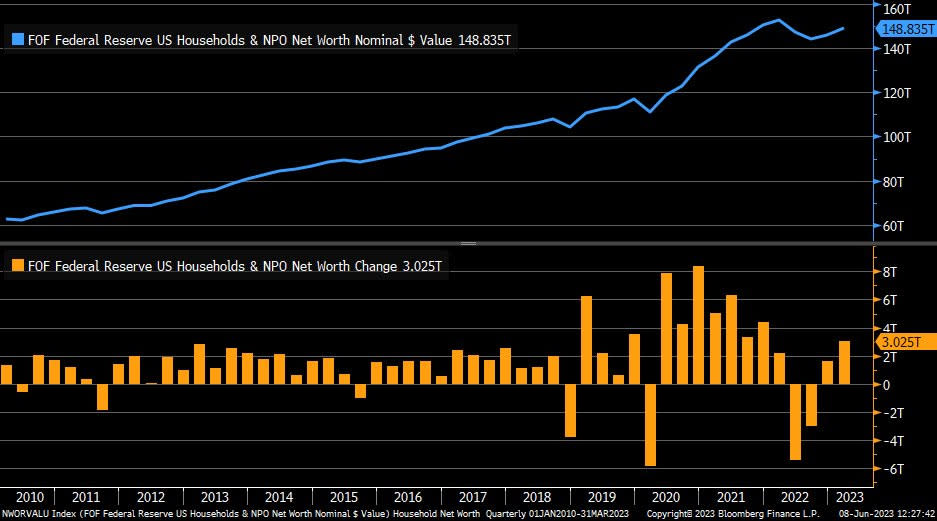

💵 Household net worth rises. Here’s Bloomberg reporting on new Federal Reserve data: “Household net worth rose $3 trillion, or 2.1%, in the January-March period to $148.8 trillion after climbing $1.6 trillion in the prior quarter, a Federal Reserve report showed Thursday. The value of equity holdings increased about $2.4 trillion in the first quarter, while the value of real estate held by households fell roughly $617 billion.”

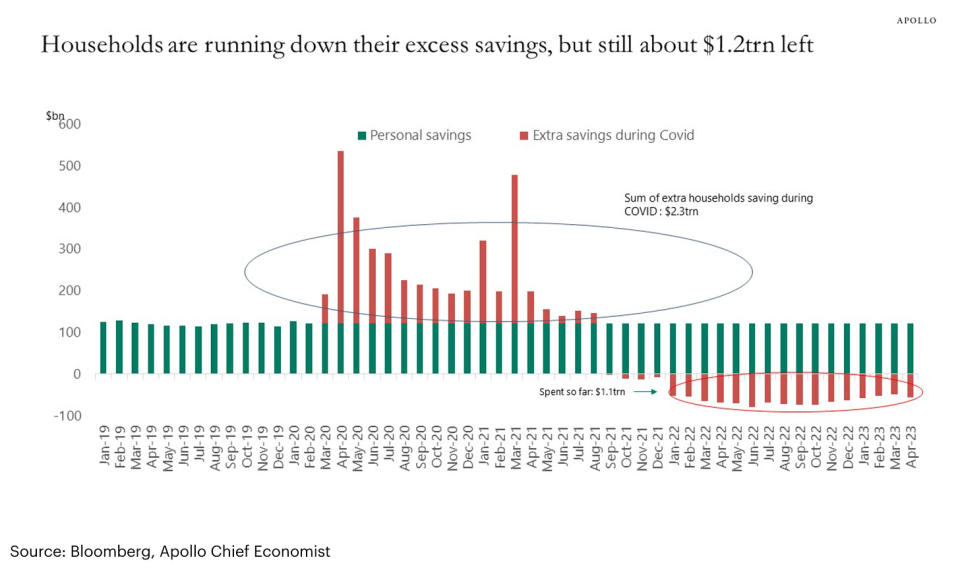

💵 Consumers have excess savings. Apollo Global’s Torsten Slok estimates households are still sitting on $1.2 trillion in excess savings.

This is a bit higher than the $500 billion recently estimated by the San Francisco Fed. Regardless, the bottom line is that consumers have a lot of excess savings, which explains why spending continues to be resilient.

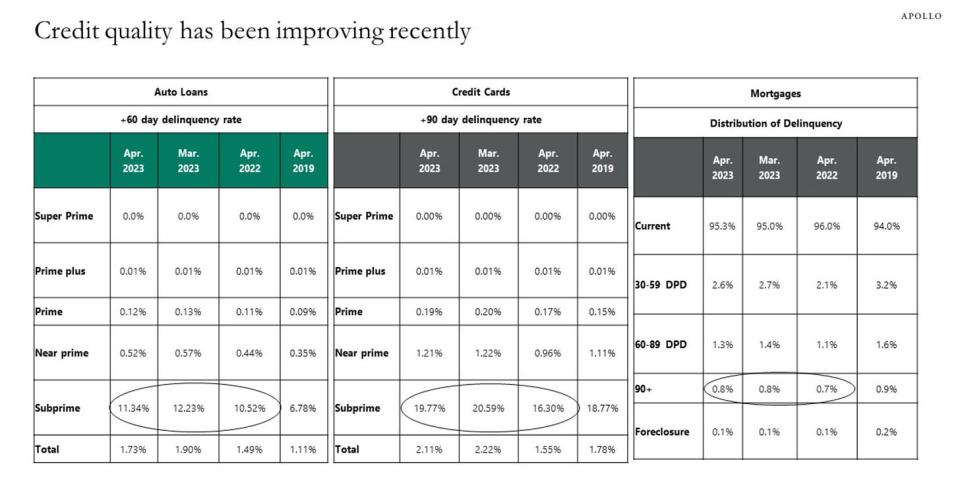

💳 Delinquency rates improve. Here’s Apollo Global’s Slok on monthly Transunion data: “The latest data shows a modest improvement in credit card delinquency rates and auto loan delinquency rates for subprime, near prime, and prime borrowers, see chart below. This is the opposite of what would be expected with the Fed trying to tighten financial conditions.”

💸 Wage growth is cooling. From Indeed Hiring Lab: “Wages and salaries advertised in Indeed job postings grew 5.3% year-over-year in May, according to the Indeed Wage Tracker. This is down considerably from the high of 9.3% set in January 2022, but still well above the 2019, pre-pandemic average pace of 3.1%.”

💼 Unemployment claims tick up. Initial claims for unemployment benefits climbed to 261,000 during the week ending June 3, up from 233,000 the week prior. While this is up from the September low of 182,000, it continues to trend at levels associated with economic growth.

From JPMorgan economists: “The move could well be distorted by the Memorial Day holiday, which is hard to seasonally adjust. Moreover, it is just one week’s move. Still, should this level persist, it would point to a more material softening in the labor market.“

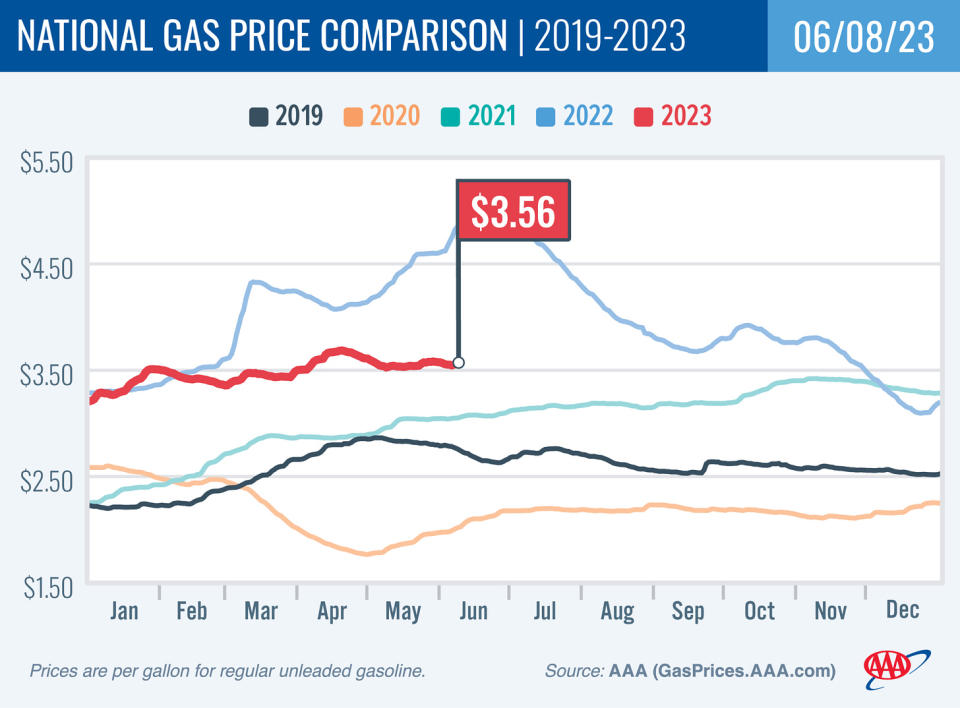

🛢️Gas prices cool as summer driving season kicks off. From AAA: “For the first time since 2021, domestic gasoline demand was over 9 million barrels daily for a third straight week. Yet despite the robust numbers, pump prices barely budged as the low cost of oil is countering a spike for now. The national average for a gallon of gas dipped a penny since last week to $3.56… Today’s national average of $3.56 is three cents more than a month ago but $1.39 less than a year ago.”

⛽️ Consumers are hitting the road. Weekly EIA data through June 2 show gasoline demand is up from a year ago.

⛓️ Supply chain pressures ease further. The New York Fed’s Global Supply Chain Pressure Index

1— a composite of various supply chain indicators — fell in May and is well below levels seen even before the pandemic. It’s way down from its December 2021 supply chain crisis high. From the NY Fed: “There were significant downward contributions from Great Britain backlogs and Taiwan delivery times. Euro Area delivery times and backlogs exhibited the largest sources of upward pressure in May. Looking at the underlying data, readings for all regions tracked by the GSCPI are below their historical averages.“

👍 Services surveys were mixed, but reflected growth. S&P Global’s U.S. Services PMI climbed to 54.9 in May, signaling an acceleration in growth. From the report: “Businesses in sectors such as travel, tourism, recreation and leisure are enjoying a mini post-pandemic boom as spending is switched from goods to services. The survey data are indicative of GDP growing at an annualized rate of just over 2%, and an upturn in business expectations points to growth remaining robust as we head further into the summer.“

The May ISM Services PMI fell to 50.3, signaling decelerating growth in the sector as new order growth cooled. Though inventories returned to growth. Also, price growth decelerated.

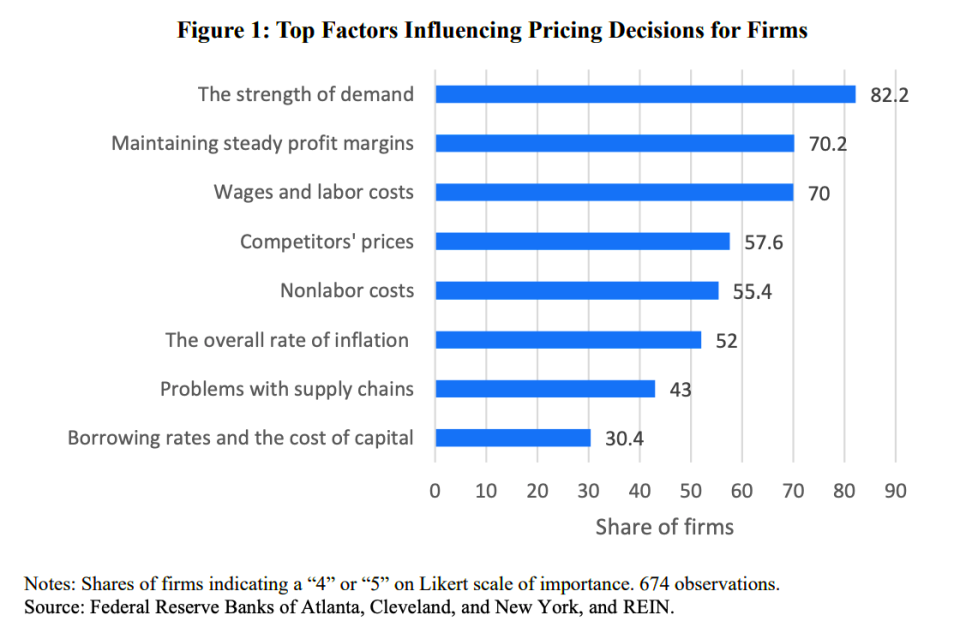

🎈 Profit margins drive inflation. A New York Fed paper (HT Tracy Alloway) found “maintaining steady profit margins” to be the second most important factor influencing pricing decision for firms.

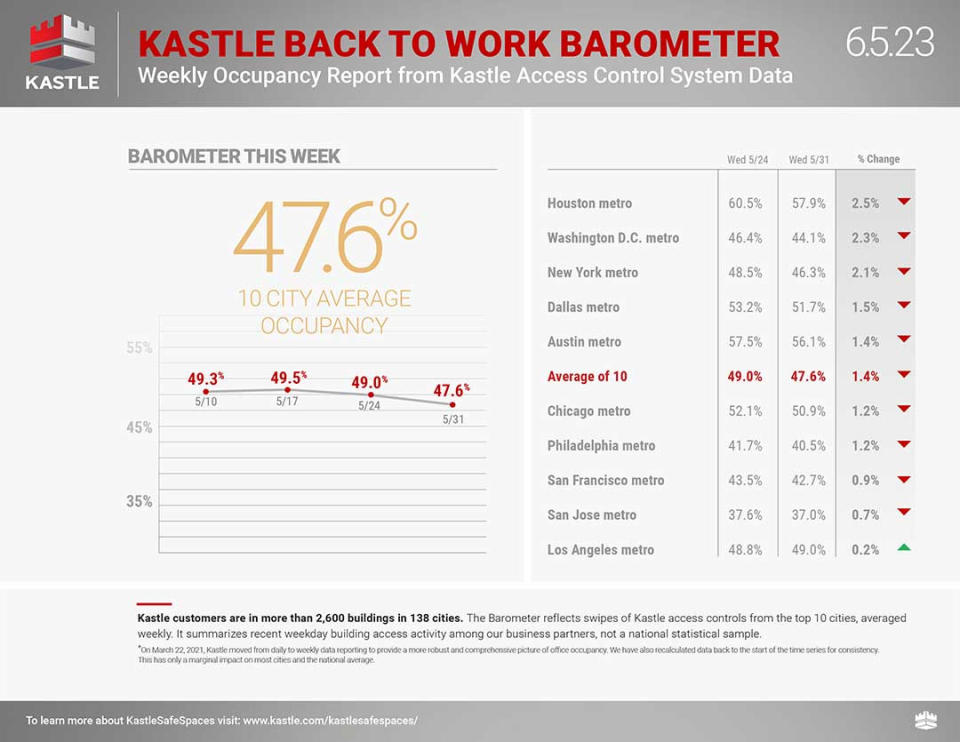

🏢 Offices are very empty. From Kastle Systems: “Office occupancy fell 1.4 points to 47.6% this past holiday week, according to Kastle’s 10-city Back to Work Barometer. The drop in occupancy was widespread, with all tracked cities seeing declines except for Los Angeles. The city rose two tenths of a point to 49% occupancy.“

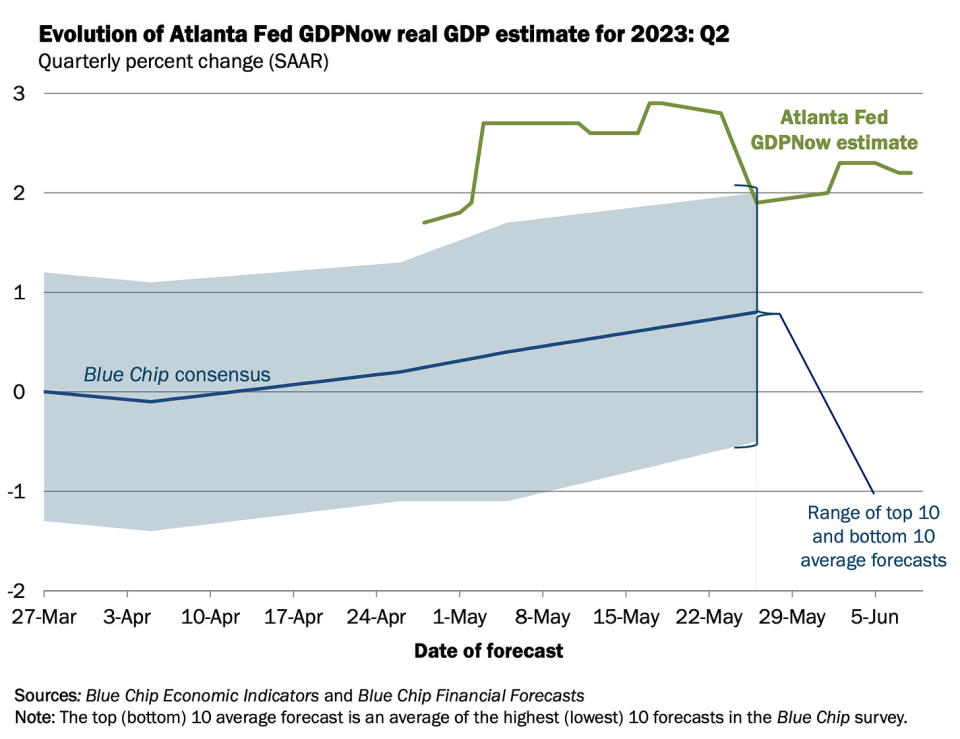

📈 Near-term GDP growth estimates remain rosy. The Atlanta Fed’s GDPNow model sees real GDP growth climbing at a 2.2% rate in Q2. While the model’s estimate is off its high, it’s nevertheless up considerably from its initial estimate of 1.7% growth as of April 28.

Putting it all together 🤔

Despite recent banking tumult, we continue to get evidence that we could see a bullish “Goldilocks” soft landing scenario where inflation cools to manageable levels without the economy having to sink into recession.

The Federal Reserve recently adopted a less hawkish tone, acknowledging on February 1 that “for the first time that the disinflationary process has started.“ And on May 3, the Fed signaled that the end of interest rate hikes may be here.

In any case, inflation still has to come down more before the Fed is comfortable with price levels. So we should expect the central bank to keep monetary policy tight, which means we should be prepared for tight financial conditions (e.g. higher interest rates, tighter lending standards, and lower stock valuations) to linger.

All of this means the market beatings may continue for the time being, and the risk the economy sinks into a recession will be relatively elevated.

At the same time, it’s important to remember that while recession risks are elevated, consumers are coming from a very strong financial position. Unemployed people are getting jobs. Those with jobs are getting raises. And many still have excess savings to tap into. Indeed, strong spending data confirms this financial resilience. So it’s too early to sound the alarm from a consumption perspective.

At this point, any downturn is unlikely to turn into economic calamity given that the financial health of consumers and businesses remains very strong.

And as always, long-term investors should remember that recessions and bear markets are just part of the deal when you enter the stock market with the aim of generating long-term returns. While markets have had a pretty rough couple of years, the long-run outlook for stocks remains positive.

")

{kind=link}