-company-has-returned-nearly-5,830%-in-just-five-years-and-is-headed-for-the-s&p-500.-is-it-too-late-to-buy?")

Perhaps the biggest business powering the markets right now is artificial intelligence (AI). It seems that every software developer is eager to cash in on AI euphoria, and technology stocks are reaping the benefits.

As the S&P 500 and Nasdaq Composite trade at record levels, my eyes have been on one stock in particular. The best part? It’s not in the “Magnificent Seven.”

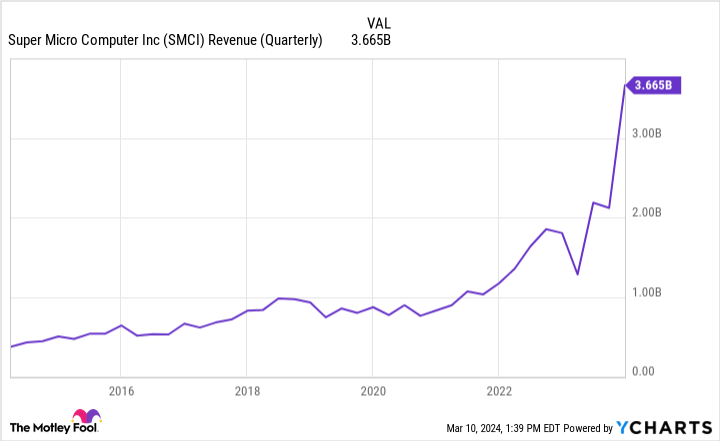

Shares of Super Micro Computing (NASDAQ: SMCI) have soared 5,830% in just five years. So far in 2024, they have risen over 300% as of market close on March 8. A lot of the momentum pushing the stock right now revolves around the company’s latest milestone: inclusion in the S&P 500.

This company is playing an important role in the AI realm. Let’s dig into Super Micro’s business and get an understanding of why the stock is going parabolic.

A superb run to the top, but…

Super Micro plays a crucial role at the intersection of semiconductors and artificial intelligence (AI). The company designs integrated systems for IT architecture, which could include storage clusters or server racks.

Given rising interest in graphics processing units (GPUs) from the likes of Nvidia and Advanced Micro Devices over the last year, Supermicro’s services have been in high demand in the background.

Revenue is growing over 100% annually, and AI tailwinds make for an encouraging long-term outlook. It’s no wonder one Wall Street analyst has referred to Supermicro as a “stealth Nvidia.”

As with all businesses, there is more to the picture than sales acceleration — as great as it is at the moment. Let’s look at some other factors to hone the full investment thesis here.

…there are some lingering concerns

One of the most important things for investors to understand is that Supermicro is very much a hardware operation, and its margin profile is much lower than you might think.

For the quarter ended Dec. 31, gross margin was 15.4%. This represented a decrease from the prior quarter and the same period in the previous year. Management addressed the margin deterioration during the earnings call, explaining that aggressive investments in new designs and market share acquisition were the culprits.

Spending to grow is an argument that only goes so far. In the long run, Supermicro will have to prove that margin expansion and consistent cash flow are achievable.

Valuation is becoming disconnected from fundamentals

Given the role of semiconductors in the AI revolution, it makes some sense that stocks such as Nvidia and AMD are garnering attention. However, Supermicro’s close affiliation with these chipmakers has brought some momentum into the picture. This dynamic can carry a lot of risk, as investors might think they are buying into the next Nvidia.

But as noted above, Supermicro and Nvidia are very different businesses. At best, they are tangentially related. More appropriate comparisons include Hewlett Packard Enterprise, Lenovo, Dell, and IBM. Its stock current trades at a price-to-sales (P/S) ratio of 7, more than double that of IBM.

Not only is Super Micro by far the most expensive stock among this cohort, but the other companies mentioned above have more prolific businesses all around. It is an extremely specialized operation and is not as diverse as IBM or Dell, for instance.

I see it as an interesting way to invest in AI. The company operates in an important pocket in the AI landscape, albeit one that is under the radar.

But with low margins and an expanding valuation, the stock’s premium appears to be increasingly less connected from fundamentals. While inclusion in the S&P 500 is a respectable milestone, it’s not reason enough to chase the stock even though it may soar in the near term as ETFs and passive funds that mimic the index rebalance their portfolios to include the new stock in the index.

For now, I would sit on the sidelines and monitor the company’s performance. If Super Micro Computer is going to be an influential component of the AI narrative in the long run, investors will have ample opportunities to buy at more appropriate valuations.

Should you invest $1,000 in Super Micro Computer right now?

Before you buy stock in Super Micro Computer, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Super Micro Computer wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of March 11, 2024

Adam Spatacco has positions in Nvidia. The Motley Fool has positions in and recommends Advanced Micro Devices and Nvidia. The Motley Fool recommends International Business Machines. The Motley Fool has a disclosure policy.

This Artificial Intelligence (AI) Company Has Returned Nearly 5,830% in Just Five Years and Is Headed for the S&P 500. Is It Too Late to Buy? was originally published by The Motley Fool

")

{kind=link}